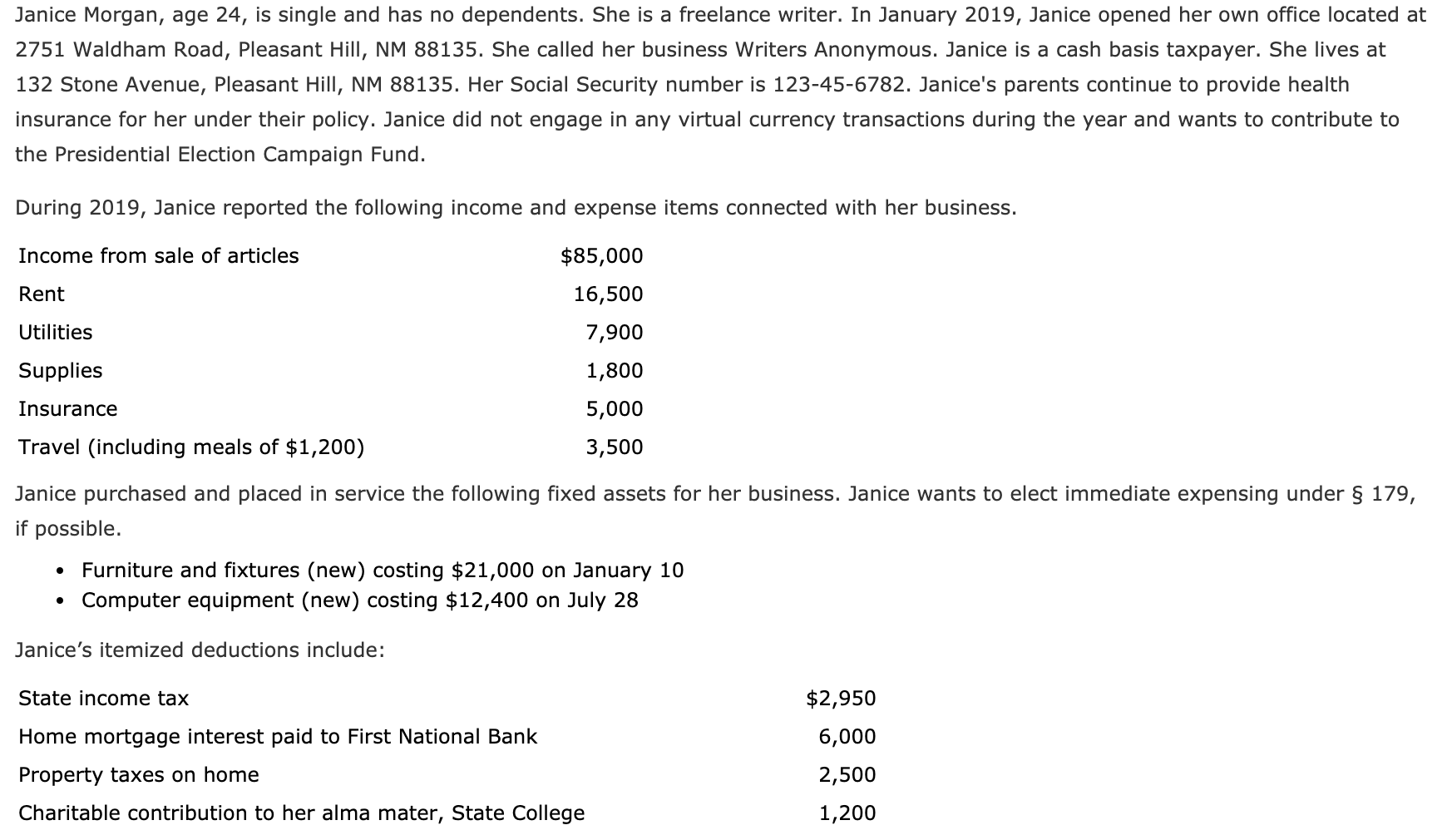

A home collateral loan lets property owners to borrow on the fresh collateral he’s in their home, or even the difference in whatever they owe on their domestic and exactly what their home is worth.

Therefore, need some cash and most it. Maybe you have medical expense to blow, otherwise college tuition debts to suit your college students. Maybe you must upgrade, redesign or create repairs to your residence. Whatever the reasoning, you have been curious whether or not a home equity loan is useful to own you. Including that loan you will enable you to use most money, and because it might be secure by the home, it’d become better to get than just a personal bank loan.

But, one which just name your large financial company, you should know brand new particulars of these types of economic facts. Exactly what are household guarantee fund, as well as how perform they work? Which are the pros, drawbacks and selection? And you may do you know the how do i include oneself as well as your family members when taking away property collateral mortgage? Keep reading to understand the fresh new remedies for such questions, and more.

What is actually property Collateral Loan?

A house guarantee loan is largely a type of financial. Such as the mortgage your grabbed aside once you purchased your house, property security loan try protected by the home itself.

Residents can also be and you will carry out fool around with family equity funds to fund solutions, condition, home improvements and developments to your family. By using a house collateral financing to cover certain household advancements, you may be in a position to subtract the interest from your own fees. not, once you have the bucks, you could do whatever you require with it purchase your own kids’ college, initiate a business, otherwise get an additional possessions, such as for instance.

How do Domestic Guarantee Money Works?

A property security loan usually allows you to obtain anywhere between 80 so you’re able to 85 % of difference between what you owe to your your house and you will exactly what it is well worth. Like, if your home is well worth $three hundred,100000, and also you are obligated to pay $100,000, you should be in a position to obtain to 80 to 85 per cent of your huge difference or around $160,100 in order to $170,100.

Although not, property equity loan is actually the next mortgage, and it’s really arranged same as a purchase mortgage. You will have to set up a software plus bank often assess your ability to repay the borrowed funds. You are able to spend settlement costs, plus house usually contain the mortgage. Possible create monthly installments over a fixed https://cashadvancecompass.com/installment-loans-oh/nashville/ number of years, however your rate of interest are fixed into lifetime of the borrowed funds. Home collateral money try amortized, for example for every commission wil dramatically reduce each other a few of the appeal and several of your own prominent of one’s loan.

Pros and cons out of Domestic Guarantee Loans

Like any other loan device, house security finance has their pros and cons. It is essentially pretty very easy to rating a house collateral financing, because they are secure by the house. Rates are usually much, much lower than he or she is getting playing cards, credit lines and private finance, so if you’re already expenses a minimal home loan rate, you don’t have to threaten by using a profit-aside refinance. Money are identical every month, very they might be simple to fit into your finances, and you will closure a property security financing is actually quicker than simply a funds-away refinance.

not, house guarantee funds are rigid you must just take a lump sum payment of money at once, that will be inconvenient if you need to use the dollars incrementally, including getting college tuition costs otherwise a restoration project. It is possible to pay focus on the currency even when you aren’t currently deploying it. Home collateral funds may also depict extreme debt, and additionally they incorporate settlement costs and you may charge. Needless to say, because your home secures the mortgage, you might eliminate your property or even pay it off.

Solutions to help you House Collateral Funds

As an alternative to traditional home guarantee finance, of several banking institutions now promote home guarantee personal lines of credit, otherwise HELOCs. In lieu of choosing a lump sum inside the a quantity, you can buy accepted to own a maximum amount of offered credit, and just obtain what you need up against one to count. An effective HELOC now offers far more autonomy if you would like spend the money incrementally, or if you or even have to obtain several times. By doing this, you pay interest toward money you probably invest. It’s also possible to manage to make shorter monthly payments in the the start.

Cash-aside refinances is actually an alternative choice to possess property owners whom realize that its residence is value a lot more than it are obligated to pay. This requires taking out home financing for more than you borrowed and you may pocketing the difference. It is advisable if you’d like an enormous sum of money to have home improvements, home improvements, college tuition, or any other expenditures, and it may end up being particularly of use as much as possible safer a reduced home loan rate.

How exactly to Cover On your own as well as your Family relations When taking a house Collateral Mortgage

A property collateral loan are going to be a wonderful equipment, but a wise resident uses warning when wielding they. Just like a home loan, you need to research rates to find the best costs before choosing good financial.

Before you take away a house guarantee mortgage, make sure you understand the words. Usually do not obtain more you might pay back, and do not create higher monthly installments which might be unsustainable. If you choose good HELOC in lieu of a property guarantee financing, be mindful; particular HELOCs need the borrower so you can use at least matter, if they are interested or otherwise not. Naturally, you could nevertheless build including a plan be right for you, so long as you feel the abuse to blow straight back the brand new difference between what you need as well as the minimum amount borrowed.

First off, do not beat your property such as for instance an automatic teller machine. It can be tempting, specifically which have a good HELOC, just to keep borrowing money. Your residence can be a means of building riches, and you will continuously borrowing from the bank against your home collateral undermines that. Make use of your household guarantee in manners that will help you expand or manage your personal along with your family members’ riches (such as by funding improvements, renovations, repairs, or even the purchase of a whole lot more assets) or their potential to create wealth (such as because of the financing higher education, otherwise carrying out a business).

Whenever you are a homeowner, you are sitting on a way to obtain cash to pay for major expenditures in the form of your home’s collateral. However,, while family equity is going to be a great capital, it’s important to understand what you are getting into with a beneficial house equity mortgage, which means you try not to end up regretting a moment mortgage.

No responses yet